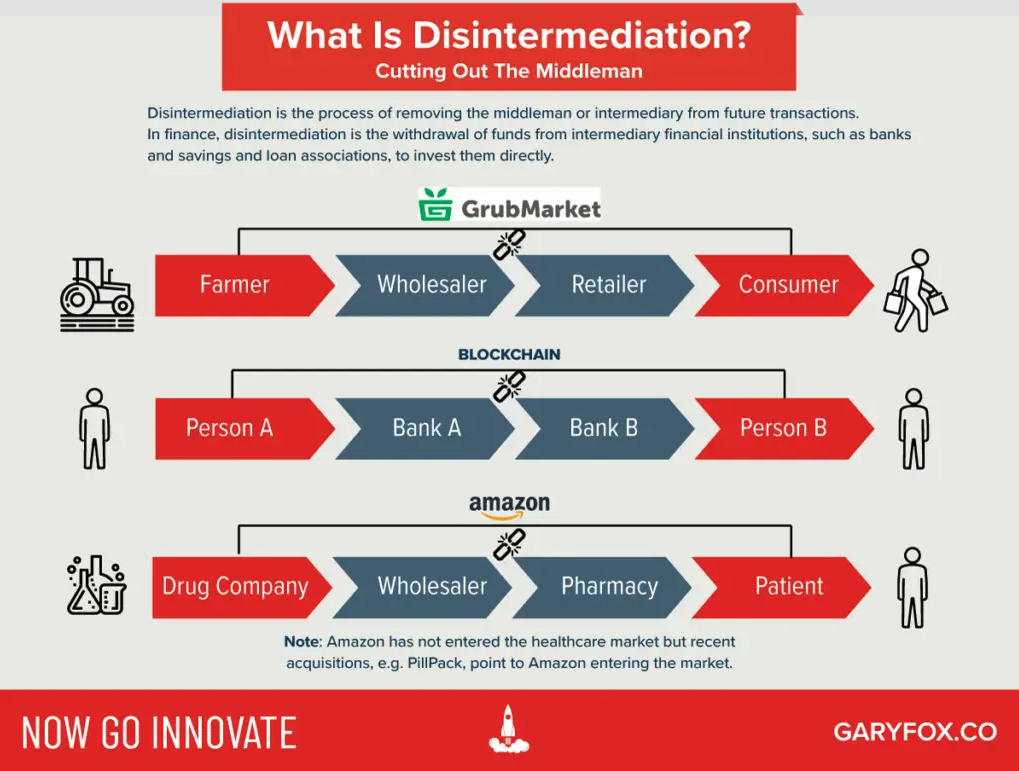

What is disintermediation… or perhaps a better question is: why don’t we see more travel agents? Disintermediation is an overly long word to describe the cutting out of the middleman, often by selling your product or service direct to the consumer. By removing steps from the value chain of a product or industry, you remove the profit that, for example, a wholesaler would make. These gains then either accrue to the seller or are passed on to the end purchaser, the consumer, in the form of lower prices. These lower prices encourage the consumer to keep using the new disintermediating platform.

How much is kept or given away depends on the competitive landscape of the disintermediated industry. Often disintermediating companies will run at a loss in order to gain enough market share and power to reap substantial profits further down the line.

Ecommerce, by its nature, leads to disintermediation. An always online connected world offers multiple opportunities to bypass traditional customer channels and sell directly to customers or through a dominant online marketplace like Booking.com, Amazon or Spotify. Commerce is no longer constrained to physical shops, while information is readily available, making consumers better informed and offering them greater choice. Why go to a travel agent with limited holiday offerings when you can book a cheaper holiday, anywhere in the world, online? Canny travel agents facing extinction are thus converting themselves to become niche recreational or social life enablers!

‘Ecommerce Will Lower Barriers and Competing Brands Will Rise’… False!

In an article on challenges facing L’Oreal’s new CEO, the Economist recently noted:

“Another threat comes from new rivals. The rise of e-commerce and social media means launching a beauty brand no longer requires complex distribution and mammoth advertising budgets. That has lowered the barriers to entry for wannabe competitors. L’Oréal, used to featuring celebrities in its advertising campaigns, now has to compete against such influencers launching their own beauty ranges”.

The threat from younger (often private equity funded) challenger brands touted by celebrity influencers is not new. At Dominion we were writing about this more than five years ago. Kardashian brands are cited as an example of a winning challenger, but in fact, they are the exceptions and if precedents are anything to go by, one that is probably short lived.

The average life of a celebrity brand not taken out by major competitors depends on the duration of the celebrity status of its founder, which seldom lasts more than a few years. Victoria Beckham’s fashion line never made a profit. Top influencers can now earn $500,000 per Instagram post without taking any business risk. Little wonder that most socially savvy teenagers aspire to being influencers!

The threat cited by the Economist has thus proved illusory (though it has allowed some private equity investors to cash out on ‘promising’ brands). The share prices of the major cosmetic brands have increased 2x faster than smaller disruptive challenger companies. The rate of share price rises accelerated once the majors refocused on developing and building out their own brands. Building a durable brand is hard, and even harder today in the age of ecommerce driven disintermediation. This is because you must compete for attention online where there is near infinite shelf space and a much more fractured media landscape.

Brand Value and wholesale are increasingly incompatible

All major fashion brands are accelerating the downsizing of their wholesale retail exposure. COVID accelerated the process but as we come out of COVID it is increasingly clear that it is not reversing. Outsourcing inventory risk to third parties like department stores and online wholesale retailers was once perceived as a valid solution to accelerating the growth in a brand. But it is now perceived as a greater risk to pricing power, given aggressive wholesaler promotions to offload stale stock in promotions to drive store footfall or more website clicks. This impacts consumer brand perception and the willingness to pay full price. Control of distribution is viewed as key, especially as it now brings with it customer analytics and fits with a brand’s desire to expand ‘Direct to Consumer’ dialogue.

Tier-1 traditional luxury brands currently control two-thirds of their distribution. Premium sportswear and cosmetics brands are following this example, setting goals for more than half of their sales to be sold direct to consumers by 2025. This is also happening online, with brands opting for E-Concessions (virtual shops within virtual shops, where the brand owner determines pricing).

Department stores have been in decline for more than 20 years and this process will be accelerated by disintermediation. Multi-brand online stores may also find themselves bereft of lucrative premium brands to sell. Nike has announced its withdrawal from ‘non-strategic’ distributors. Fashion e-tailer strategies are polarising as a consequence. Some are bulking up on digitally native own brands (ASOS), while others are abandoning own brands to offer platform services (warehousing, logistics and marketing services) to partners while retaining the traditional wholesale model of buying goods and then having control over how they are sold. Whether online or offline, multi-brand stores will need to have some kind of draw for customers to survive. It could be platform leadership, additional services, logistical fulfilment capabilities or even an experiential aspect (tourist attractions or resorts in the case of the holiday market).

Not all disintermediaries succeed

The lure of outsized profits from a platform that will successfully disintermediate an industry generates a lot of excitement and high valuations. But investors can lose when investing in companies that have not yet even proven their disintermediation ability or are just traditional retail models pretending to be disruptive platforms.

A great, or rather nefarious, example is the UK property portal Purple Bricks. The company aimed to remove the commission element of house buying, a strong consumer offer, in the hopes of getting enough listings that its site would be the ‘go to’ location to look for houses. While the company managed to accrue a decent amount of market share it never reached critical mass. It was not a platform business model. This meant that it still had to hire real estate agents to show and market houses, but its pricing model meant it seldom, if ever, was able to hire the best quality staff. Thus, the company became just another estate agent (albeit one without an office) all the while still paying fees to the true disruptor of the UK housing market: Rightmove, a company that provides a unified place for housing listings and advertising with 83% market share. Purple Bricks is yet to make a profit while Rightmove enjoys 65% operating margins.

The key to disruptive disintermediation is not to replicate a prior industry with online characteristics, but rather to form a platform that benefits from capital light network effects. Rightmove in the UK and ImmobilienScout in Germany enjoy a symbiotic relationship with real estate agents who are their biggest clients, which has resulted in both parties thriving (great news for investors) and which has acted as a major barrier to entry to hopeful me-too disruptors. In short “Adapt, if you can’t beat them, join them”.