Market timing does not work. So what should investors do?

Waiting for the perfect moment to invest in equities is like Waiting for Godot...

Hesitation Kills

In August 1776, during the American Revolutionary War, George Washington was leading the defence of New York. A much larger British force had George Washington and his army of 19,000 men pinned against the East River and surrounded on all other sides. Decisive victory was close-at-hand for the British. It was at this decisive moment that the British commander, General William Howe, hesitated. Instead of pressing home the attack and inflicting a great defeat on the American revolutionaries, potentially ending the war with British victory, he waited. This allowed the Americans time to get most of their army across the East River and to safety under the cover of darkness. If General Howe had been more decisive the course of history would have been very different. His hesitation was driven by a desire to wait for a better opportunity to attack, an opportunity, like Godot, that never arrived. General Howe’s hesitation cost him victory.

In the case of equity investing, many investors today remain underinvested or have no investment exposure to equities. This is a market timing decision and has parallels with our previous examples of General Howe and Beckett’s Waiting for Godot. Investors choosing to have no exposure to equities and hold cash (or other assets) are making an active market timing decision. Those investors are choosing to avoid equities in expectation of a future moment that will offer them a better opportunity to invest. Like General Howe, they are waiting for the perfect opportunity to arrive. However, like Godot, this opportunity may never show up.

Many investors think the current market rally may have run too far, or we may have another recession on the horizon. Others point to the challenging global political environment as an argument for steering clear of equities, hoping for a better moment in the future to invest. The truth is that such a moment in the future, a gold-plated ‘Invest Now!’ moment in equities, will never arrive. And in the meantime, equity markets will continue to power ahead and investors attempting to time the market will be left in the cold. Time and time again, research1 from the world’s leading academic and financial institutions has shown that market timing is a (very) bad choice for investors.

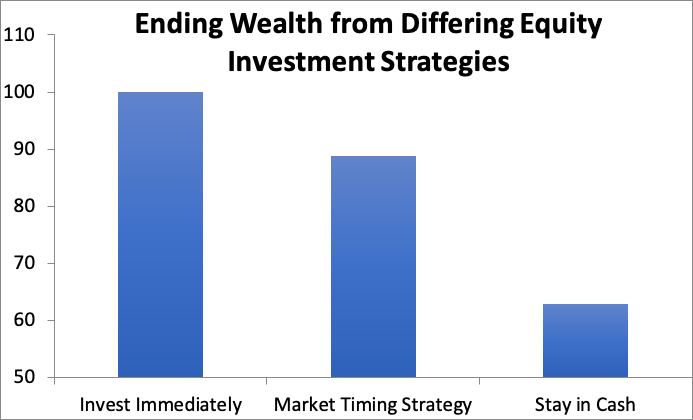

An example of research proving that market timing is a bad strategy is shown in the chart above. This analysis from a Charles Schwab research project shows the investment outcomes from three investment strategies, modeled over a 20- year period in equity markets. The modeled portfolios assume $2,000 of annual investments over the period. What we see is that investing each $2,000 amount every year immediately into equities and remaining fully invested generates by far the best investment returns for the investor. The attempt to time the market led to significantly weaker investment performance, while the worst performance was from the portfolio that avoided equities and remained invested in cash (another form of market timing). The most proven and highest return strategy over time has been shown to be one where investors do not try to time the market at all. ‘Invest and remain invested’ has been proven over decades of research to be the optimal strategy for investors with the highest returns. The evidence shows that investors should not hesitate with their investment timing and that by hesitating they risk missing out on the significant upside from equity investing over the long-term.

1 For further research see: (i) Metcalfe (2018) ‘The Mathematics of Market Timing’

link: https://journals.plos.org/plosone/article?id=10.1371/journal.pone.0200561

(ii) Johannes, Polson, Stroud (2002) ‘Sequential Optimal Portfolio Performance: Market and Volatility Timing’ link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=304976

(iii) Dellva, Demaskey, Smith (2001) ‘Selectivity and Market Timing Performance of Fidelity Sector Mutual Funds’ link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=274415

What about China macro-risk, trade wars, Brexit, Donald Trump, North Korea....

Compounded growth in corporate profits, management teams at top companies driving growth in your equity, the global economy powering ahead and driving growth in equity markets. These are powerful forces and investors would be wise not to avoid them. The modern global economy has survived two world wars, depressions, the threat of communism, financial crashes... and it has come out of all them stronger and more productive than ever.

Are things that bad now?

Let’s take a worst-case scenario from the past 80 years as an example of why investors should remain fully invested in equities. In 1941-1942, the Second World War was raging and it was going very badly for the Allies. The Axis Powers, Nazi Germany and Imperial Japan, were on the offensive everywhere and controlled vast swathes of Europe and Asia. It is hard to imagine a more risky time to have the confidence to invest in equity markets. However, if an investor had done just that and remained invested in equity markets with a $10,000 investment in 1941, today that investment would be worth $42.9 million. Over the long-term, investors remaining fully invested in equities benefit from compounded growth of profits, dividends and investment returns. Patience truly is rewarded and investors attempting to time the market risk missing out on this long-term opportunity. The above example helps to put our current predicament in global markets into context. Our concerns about Chinese economic growth, Brexit, or President Trump’s next tweet, pale into insignificance compared with the world that faced investors through most of the 20th century. Those 20th century investors who remained fully invested in equities, even during the riskiest periods of that century, were very richly rewarded.

What about when markets are going down?

Once again, taking a long-term view is very helpful for investors here. Think of a short-term equity market decline as being like turbulence on your next flight. Many commercial air flights can encounter turbulence on the way to their destination. Sometimes this turbulence can be quite severe. But would any investor reading this article, when encountering turbulence on their next flight, use that as a reason to grab a parachute and jump out of the plane?

Wait... don’t jump!

No! Turbulence on a flight is nothing more than a bump on the path to a longer-term destination. Market corrections are much like turbulence on a long-term trajectory to higher equity markets. They are part of the normal pattern on a journey to the long-term destination of a larger global economy and higher equity prices. Investors must be brave during these inevitable periods of turbulence in markets, and should not jump out of the exit! In his masterful poem ‘If’, Rudyard Kipling begins with: “If you can keep your head when all about you are losing theirs.” This is apt advice for investors facing a period of weak equity markets. For those investors with equity investments, choosing to do nothing when markets are falling is a hard thing to do. ‘Keeping ones head’ as Kipling might have put it, is the difficult but correct thing to do.

Periods of market declines are part of how markets operate. Equity markets and equity fund performance may be negative for periods lasting months. This was the case in 2018 (and 2016, and 2011, 2008, 2001, 1990...). In fact we have a very long-track record of equity markets declining for short-term periods. Declines happen and investors in equity markets should expect them to keep happening in the future. It would be very strange if they did not happen. The important thing for equity investors is what to do during a market decline. The answer is simple, but hard to do in practice: do nothing! Responding to weak markets by exiting investments is a form of market timing. You are making a prediction about short- term market performance and as we have discussed, this has been proven, time and again, to be the wrong strategy.

If the global economy can power through the threats it faced in the 20th century, then today’s challenges are nothing more than blips, which will be long forgotten in the future. Investors must be careful not to catastrophise, putting too much emphasis on the problems in the world today (hint: there are always problems in the world) and missing the great opportunity offered by investing in equities and the growth of the global economy over the long-term. Taking a long-term view of the past helps us to understand how robust the modern global economy truly is. It is a powerhouse of unprecedented wealth creation and equities as an asset class offer the optimal exposure to this growth engine. Knowing, as we now do, that market timing doesn’t work, there is a very strong case that investors should look to maximize their exposure to equities for the long-term and remain fully invested.