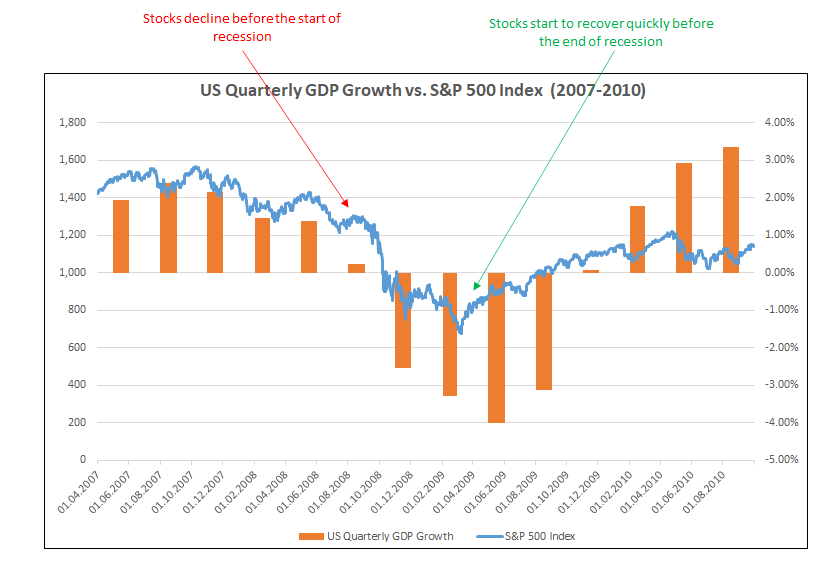

Markets discount the future. The track record of bond and stock markets moving ahead of economic data is very strong over the past century. Data sets like GDP and unemployment are often late to the party, showing major changes in direction well after markets have started to price this outcome. During past economic downturns, we have seen markets move down months before we start to see negative GDP growth or major increases in unemployment.

Below we show the S&P 500 Index (in blue) and US Quarterly GDP growth rates (in orange). This period is 2007-2010, which was the last recession in the US. You can clearly see here that stocks start to move down before the recession starts (GDP goes negative). This is a similar pattern repeated in recessions before 2007-2010. The market discounts the future by pricing in a weaker economy before the headline data weaken.

This cuts both ways. Markets also typically start to price in economic recoveries well before the headline economic data improve. Again, looking at the 2007-2010 recession, we can see clearly that the stock market recovery starts early, before the GDP growth rate increases.

When the news is getting more and more negative about the economy, this is good timing to start adding to equity exposure, because the recovery in prices will usually start before the end of the recession is announced in mainstream media, or shows up in the headline GDP data.

If you wait for the good news, it may be too late and you have missed most of the recovery in stocks.