Why the future may not be so bright for equity ETFs and why actively managed strategies may offer investors much stronger returns over the next decade.

The calm before the ETF storm?

“A rising tide lifts all boats”

John F. Kennedy, 1963

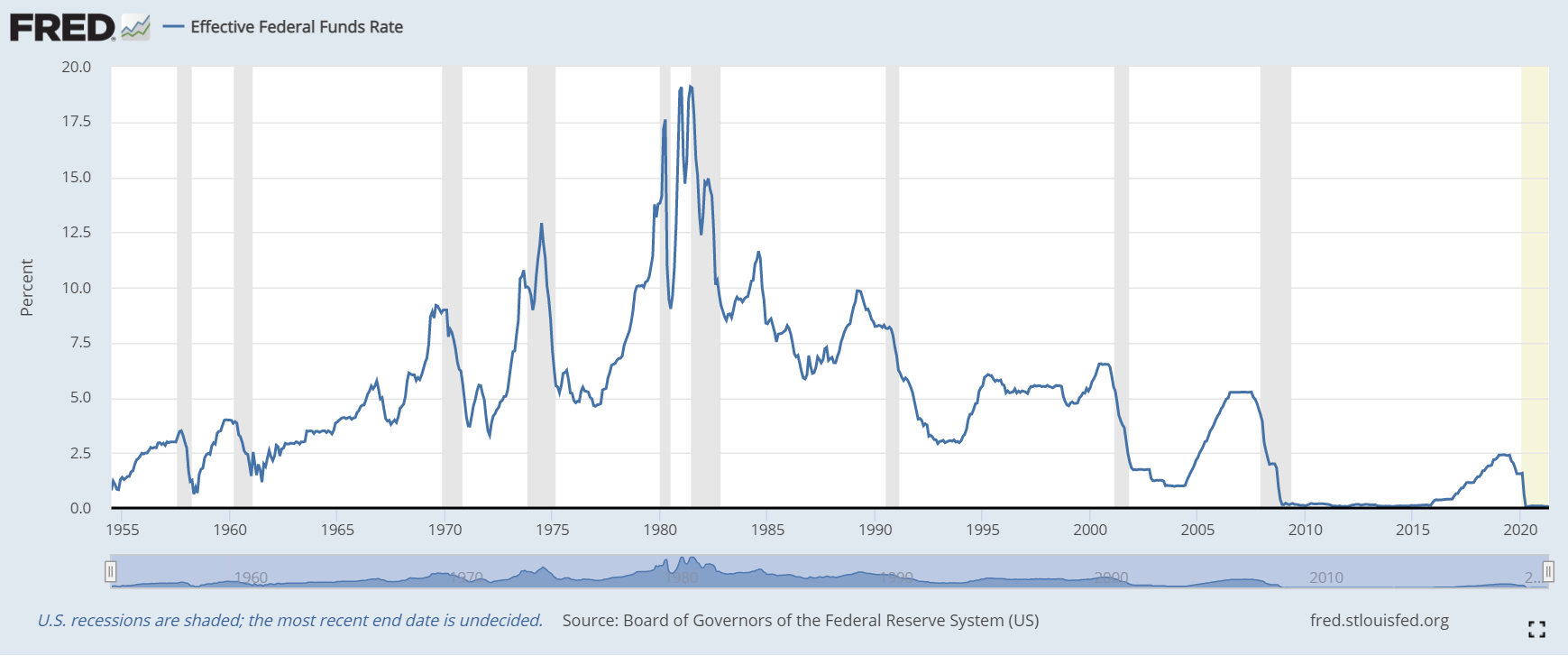

The above quote from John F. Kennedy, taken from a speech he gave shortly before his tragic assassination, is very useful in helping us understand what has happened in equity markets since 2008 and what is likely to happen next. The rising tide for equity markets was triggered by central banks and the massive monetary stimulus pumped into the financial system in the wake of the 2008 global financial crisis. Ultra-low interest rates and the printing of trillions of dollars in new money (quantitative easing, or ‘QE’) flooded global asset markets with capital. Much of that capital found its way into passively managed funds, like ETFs. In fact it was close to $7 trillion of capital that was moved into these passively managed funds between 2009 and 2020. Like the tide coming in, these trillions of dollars of capital flowing into passively managed funds has pushed up the price of everything listed on the major stock indexes these instruments are designed to track. The tail has been wagging the dog.

Investors in passive equity strategies have enjoyed a decade of strong returns and outperformance of actively managed equity funds. A $7 trillion injection of capital into passive funds will tend to have that effect! But this trend could very likely be about to end. And what is worse for investors in passive equity funds, the reversal of this trend could have dramatic negative effects for their investment returns over the next decade. We are likely close to the high tide for the passive investment flows in equity markets. The monetary stimulus that created the flood of capital into these funds will have to stop eventually. And this trend could start to reverse soon, with capital flowing out of passive funds and the performance of these strategies declining. Investors in passive equity strategies may not want to be around when the tide is going out!

To quote President Kennedy once more: “Change is the law of life. And those who look only to the past are certain to miss the future.”

What has worked in the past decade will not necessarily work in the future. Financial markets are changing. And investors must be prepared to change too...

“The Tide is High, But I’m Holding On”

John Holt, 1966 (covered by Blondie, 1980)

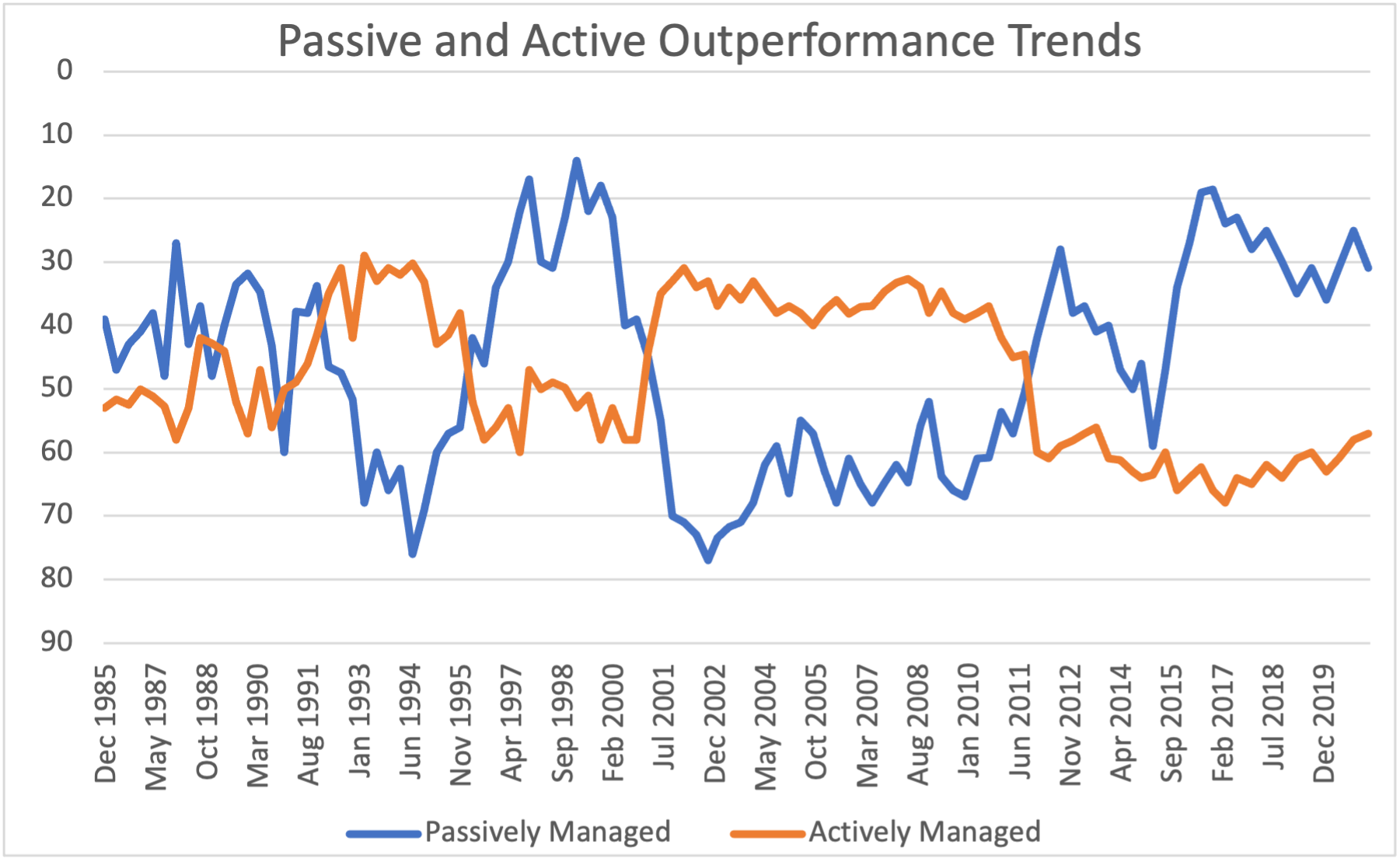

Passive equity investment strategies have delivered higher returns than active (on average) most years since 2009. Investors who picked equity ETFs and other passive strategies over actively managed equity funds have seen stronger investment returns since 2009 and might be forgiven for wanting to hold on to their investments. It has worked for 80% of the time over the last decade, why change? The reason is simple: this tremendous period of outperformance for investors in passive equity funds has been a once-in-a-generation gift, courtesy of central bankers.

Two unprecedented trends have occurred between 2009 and today. First, the world’s major central banks generated the biggest monetary stimulus in history, through the setting of ultra-low interest rates and the printing of trillions of dollars of new money. Second, asset prices in every major asset class have seen the longest and least volatile bull-market in history. The first trend caused the second trend. This monetary stimulus created massive amounts of new capital, which had nowhere to go other than equity, bond and real estate markets, pushing up the prices of all those asset classes to record levels. In the case of equity markets, much of this capital found its way into passive investment funds, like equity index ETFs. The tide was coming in and equities were trading as an asset class rather than as individual businesses with differing end market exposures and investment prospects. The past decade was characterized as one in which it was better to own index tracking funds, in other words: own a bit of everything in the equity market because everything is going up. Capital invested in passive equity funds is today at record levels as a proportion of total capital under management. This trend was into its 13th year at the beginning of 2021 and investors would be forgiven for thinking this is a new normal for financial markets, that this is just the way things are now and passive will continue to be the best way to earn returns in equities.

However, if we look at the period 1999 – 2008 (the decade preceding 2009 – 2021) we see a very different picture. In that decade, actively managed equity strategies outperformed passive funds in 8 years out of 10. Investors were much better off between 1999 and 2008 investing their capital in active equity strategies. If we look back over an even longer period (see the next chart which goes back to 1985), we find that the relative performance of active versus passive investment strategies is cyclical. We have lived through multiple periods of passive equity strategies outperforming active strategies, the most recent decade was one of those periods. But these periods are typically followed by the reverse. Long periods of active equity investment strategies outperforming passive strategies. With the steady normalization of monetary policy by central banks to come in the next 2-3 years, the fuel which powered passive fund outperformance over the past decade may soon be running out. We could very likely be on the verge of moving into a new and sustained period of active equity strategies outperforming passive strategies.

The relative performance of passive to active strategies is cyclical and we appear to be at the top of the passive outperformance cycle. The next decade could be defined by actively managed equity funds outperforming passive funds and those investors exposed to products like indexed ETFs should be prepared to adapt to a new environment where actively managed strategies take the lead and passive strategies underperform.

“Only when the tide goes out do you discover who’s been swimming naked”

Warren Buffett

2020 was an important inflection point for financial markets. The regime of monetary policy support went into overdrive to support markets and the economy through the pandemic. This will eventually have to be reversed to restrictive monetary policy and central bankers are already talking publicly about this. Rising inflation will be the likely trigger. The monetary pump driving $7 trillion of capital into passive equity funds over the past decade may likely be switched off, and soon. The 2009 – 2020 period will be remembered as one dominated by unprecedented capital flows into passive funds, which in turn pushed up the prices of virtually every stock listed on major stock indexes, irrespective of the underlying fundamentals of those companies. The true value of stocks relative to each other has been hidden by this trend of buying everything, in fact many stocks that happen to represent a larger proportion of indexes (due to the size of their market capitalization) have outperformed simply because they are bigger and so more of their shares have to be purchased when there are inflows into passive funds.

The ETF investment tide could soon begin receding and investors should be aware of the potential risks of not adapting to the new investing environment we find ourselves in today.

A reversal in the trend of capital moving into passive equity funds means those funds will have to indiscriminately sell stock in the constituents of stock indexes those funds are designed to track. As these funds are passively managed, there is no active management team to decide on what to buy or what to sell. Given the record levels of capital now invested in these passive instruments, a significant shift of capital out of these funds could have a dramatic downward pressure on the performance of passive funds as an asset class, particularly if there is heavy selling of these instruments and liquidity tightens.

Even if we take a more optimistic view and assume there is no reversal in capital flows, the outlook for passive funds is still not great. Let’s assume the capital that has moved into passive funds stays put and does not look for a new home. Passive returns are still likely to underperform the returns of active funds, especially active funds with strategies focused on buying a portfolio of stocks with attractive valuations and strong long-term growth exposures. The primary ‘push factor’ pushing up prices of ETF index constituents, and therefore the performance of ETFs, will eventually go away. The only buyers and sellers left in the market, on a net basis, will be active managers looking to pick the winners and sell the losers. After a decade in the wilderness, actively managed capital is going to start deciding the investment returns of equities and passive strategies will have a diminishing impact. This will favor those equities with more attractive valuations and stronger long-term growth prospects.

The Chinese use two brush strokes to write the word 'crisis.' One brush stroke means ‘danger’, but the second means ‘opportunity’. In other words, in a crisis be aware of the danger but also recognize the opportunity. The new global regime for financial markets may seem scary to investors who have gotten used to steady returns from passive equity instruments. But this change offers investors a great opportunity to make a once-in-a-generation shift to overweighting their exposure to active equity funds. In particular it will be those funds that offer investors exposure to fundamental growth trends in the global economy that could see the most attractive investment returns over the next decade.

A Lesson from History

The Great Sioux War of 1876 may not be the first place that investors look for lessons on how to approach investing in equities in the 21st century. However, there is at least one lesson from this conflict which offers investors some very useful insight today.

General Custer’s defeat at the Battle of Little Bighorn is one of History’s great examples of overconfidence and a failure to adapt. Custer’s failure to understand the situation he was in, his overconfidence that what worked for him in the past would work again, and his underestimation of the risks he faced led to a disastrous military defeat at the hands of a coalition of native American tribes.

General Custer had a career in which he had gotten used to winning. Serving in the US Civil War and in later conflicts, he was always on the victorious side of the battle and expected to keep winning without adapting. Custer’s successes up until 1876 likely fed into his high confidence that ‘doing the same thing again’ would win the day.

The lesson for investors today is that they must be prepared to adapt if things change. Relying on what happened over the past decade to keep happening again can lead to disaster.

We at Dominion are confident that the future is brighter than ever for our investment strategies. Our investment funds offer long-term investors exposure to actively managed equity portfolios, focused on buying attractively valued companies with the best exposures to growing revenues and profits.

We view the current changes underway in global financial markets as being a benefit to our strategy, clearing the way for actively managed capital to pick the long-term winners in the global economy and avoid the losers. While the last decade was characterized by capital flows into ETFs driving share price performance, we firmly believe the investment returns of the next decade will be defined by investing in a limited number of the best companies offering the most attractive exposures to long-term growth.

Investors should avoid the mistake of assuming the past will simply repeat itself. Passive investing looks to have peaked, with future outperformance looking unlikely. The next decade is more likely to be one where investing in actively managed strategies, with exposure to the best companies and highest growth trends in the global economy, once again becomes the optimal strategy for equity investors.