Investing in legal cannabis has become a big trend in recent years, but reality has yet to match raised investor expectations. The DGT Luxury Consumer Fund offers investors exposure to this trend without the high risk of investing in “hype” stocks.

“Don’t Believe the Hype” – Public Enemy, 1988

The emerging legal cannabis industry has become a hot investment trend in recent years. Billed by many investment research writers as an “end to prohibition” moment, the investment thesis for cannabis looks great on paper when viewed from the top down. The legalization of the recreational drug will be, say the bulls, like the repeal of prohibition of alcohol in the United States in 1933. Following the repeal, the large black market created by the prohibition of alcohol quickly came into the light and became a legal private sector industry. The widespread black-market supply of cannabis, the bulls argue, will quickly become a new legal private sector supply chain, offering investors an immense opportunity to invest in this newly legalized industry.

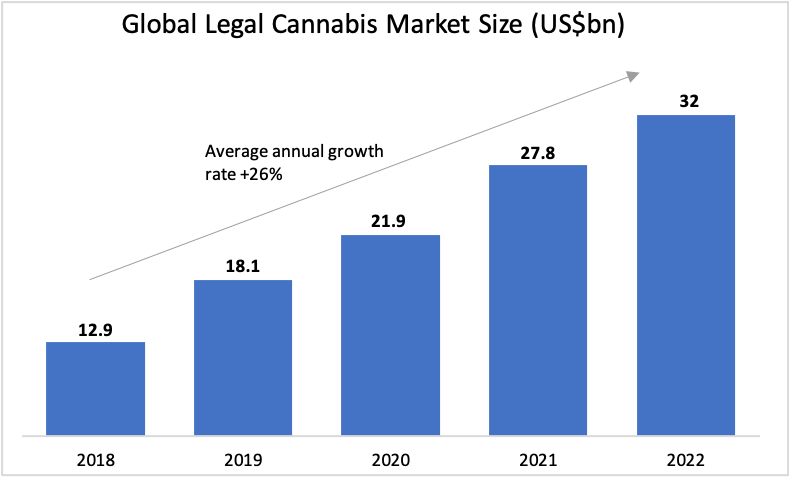

Legal cannabis industry data would appear, at first glance, to support the bull case. The global market today for legal cannabis is worth $18 billion annually as of 2019 and the market is growing at an average annual growth rate of +26%. The market is expected to reach a value of $32 billion by 2022.

But taking a closer look at the fundamentals of the legal cannabis industry shows that the bull case is not everything it’s cracked up to be (no pun intended). While the legalisation of cannabis may well be a once-in-a-lifetime moment, it is probably not a once-in-a-lifetime investment opportunity.

In the long-term, the legalised cannabis industry has strong prospects and could rival the alcoholic beverage and tobacco industries in terms of scale and profitability. Our concern, however, is that this mature state for the industry is a long way off and that current market expectations for legal cannabis are too high. This means that we will inevitably have to go through a period of deflated expectations and disappointment, with inevitable declines in share prices of pure-play legal cannabis stocks. Investors would be well advised to avoid these stocks and look for a smarter long-term exposure to this trend.

Peering through the smoke-screen

As many students can attest, an illegal and readily accessible recreational market for cannabis has existed for some time. There is very high latent demand for legal cannabis. Cannabis at the federal level in the United States has been hitherto defined as an illegal drug on the basis that it has no medicinal benefits and has the potential for being misused. Against a backdrop of accelerating measures by US States to legalise, there is a growing body of research indicating that there are medicinal benefits of cannabis use. Cannabis is a fast-growing plant which contains many molecules including two sought- after constituents: THC (Tetrahyrocannabinol) and CBD (Cannabidiol). The former is a psychoactive inducing a “high” feeling, the latter is indicated as a non-addictive pain killer, calmer and relaxant with few, if any, serious side effects. The market potential for using the drug legally in consumer products is huge.

Growth in the legal cannabis market is, however, predicated on legislation, and legislation never happens in a hurry. Legislation milestones have shaped the cannabis industry up until now. An important milestone came in December 2018 when the United States passed The Hemp Farming Act. This now allows cannabis (in the form of hemp, which has a low- concentration of the psychoactive chemical THC, which is what produces cannabis’s mind-altering effect) to be farmed as a normal crop. This generated both a growth in the supply of hemp and a ramp up of interest to research the medicinal qualities of CBD. Already now today in large parts of the United States, major health and wellness companies sell CBD cannabis-infused products at retailers like Walgreens. The spread and wide acceptance of these cannabis-based products has helped drive the hype around the potential investment returns in the industry for legal supply of the drug.

What is critical for investors looking for exposure to this trend to understand is: what determines the rate of growth of the new legal industry? The answer is simple: the rate of growth of the industry will be determined by the speed at which demand can be transferred from the illegal recreational market to the legal recreational market.

To us at Dominion, the prohibition metaphor used by those who are bullish on legal cannabis is flawed. When the prohibition of alcohol in the United States was lifted in 1933, the infrastructure to produce high volumes of alcoholic beverages legally was already in place. Prohibition started in 1920 and in the period before repeal in 1933 organised crime syndicates took over the defunct breweries, bars, and distilleries to create an alcoholic black market. This black market was supplied by the legal infrastructure that was in place before 1920.

Once prohibition was repealed, it was simply a matter of legitimate companies co-opting that supply infrastructure from illegitimate companies, and then re-labelling black market supply as legal supply, all using pre-existing supply infrastructure. There is no comparable situation for cannabis, which is where the comparison to prohibition breaks down. While alcohol had a long history as a legal product before prohibition, cannabis has no such history of being supplied at scale by the private sector. The legal cannabis industry will have to be built from the ground up, a long and capital-intensive process. That’s a very different and far longer process than simply taking control of pre-existing infrastructure and ramping up supply.

Beyond recreational use, medicinal use is a major market for cannabis. The drug is a natural painkiller which is non- addictive. Given the ongoing opioid crisis in the US, there is enormous interest in alternatives and that is driving enthusiasm for cannabis and again supporting the hype around predictions of growth and profitability in the cannabis supply chain. This medicinal interest is a worldwide phenomenon, but legislation is once again responsible for keeping it in check. While American states can legalise cannabis, the federal government, which sits above them, continues to regard it as an illegal drug. This has created a situation where US banks cannot provide banking services to foreign investors in cannabis production. This is a significant barrier to investment in new legal cannabis production capacity, which is critical to the legal industry supply-side being able to compete with the illegal supply side.

The US, the world’s largest legal cannabis market and the market with the most potential, is unlikely to see its legal cannabis market match the scale and profitability of more established markets like tobacco or alcohol for some time to come. Legal cannabis is still more expensive than illegal cannabis to produce. Producing cannabis legally and paying taxes on any profits is currently far more costly than the cost of black-market produced cannabis, a market which is already well established not only in the US but everywhere in the world. The cannabis black market has had a long time to develop an efficient and low-cost supply chain!

The only way to drive parity in price between legal and illegal cannabis is for the legal supply chain to achieve economies of scale, the same kind of economies that the legal tobacco and alcohol industries enjoy today. Illegal production of beer, for example, would struggle to come anywhere near the low cost of production of large established breweries. This process of the legal industry scaling up will happen in cannabis production, but it will take time and a lot of capital investment. When legal cannabis finally becomes cheaper than its illegal equivalent, we will see a wholesale transition of demand into legal supplies. This price differential and the barrier it creates for a quick uptake of legal cannabis on the market doesn’t just apply to America. It applies anywhere that has an established black market in cannabis... which is pretty much everywhere.

And beyond the economies of scale hurdle lies another major issue for the legal cannabis industry. How should legal cannabis be allowed to market itself? Legal tobacco and alcohol have enjoyed decades of being able to build brands and spend millions on advertising without restrictions. Advertising restrictions on those products have only started to appear in recent years. Any cannabis product requires FDA approval in the US and would likely face restrictions on advertising, not allowing cannabis companies the room to build their brands anywhere like to the same extent that tobacco and alcohol brands have been able to invest in their brand recognition.

The Dominion Approach

In the DGT Luxury Consumer Fund, we have created an exposure to the cannabis trend for investors without taking a direct investment in any pure-play cannabis supply stocks, where we see the risk of price volatility as being high. The Fund holds a position in Constellation Brands, the US’s largest premium beer company. Constellation Brands is the largest shareholder (with options for an absolute majority) in a company called Canopy Growth, the largest listed cannabis stock. Intent upon obtaining a return on its investment in Canopy, Constellation’s management has moved quickly to remove Canopy’s acquisitive “visionary” founder/CEO and has installed managers with long standing experience in building premium wine and beer brands. Constellation shares are valued in-line with premium drinks brands (FCF yield of 3%) and do not carry any premium rating for control of Canopy. Constellation generates cash from fast growing premium beer activities and pays a dividend. All major listed cannabis companies are currently bleeding cash, a situation which is unlikely to change in the short term. Expectations regarding Constellation’s growth prospects look realistic while those for the cannabis industry look too optimistic. Given the “hype” valuations in cannabis stocks, the consequences of disappointment may be painful for investors.

There is no doubt that the cannabis industry will grow enormously – but we think the number of years in question is far, far, greater than most commentators are appreciating. Undoubtedly, the demand for cannabis (both recreational and medicinal) is huge. But barriers to growth are high and at present, the major players in this nascent industry look frighteningly overvalued – especially since none of them seem to actually make any money yet!

Instead of investing in one of these companies, we have chosen to invest in a company that will control the largest legal player in the cannabis industry (Canopy). That company, Constellation Brands, is a premium beer seller, and a growth story in its own right. But it also represents a fairly-valued indirect route into cannabis for investors.

For now, we think that’s the safest way to get a piece of an industry that we don’t doubt, with time, will be huge... but which may have to go through some significant readjustments before its potential is realised.