Economic data released today showed that the US economy contracted for the second quarter in a row. Real GDP growth contracted at a -0.9% annualised rate in the second quarter of 2022. This follows a -1.6% contraction in the first quarter of this year.

Two quarters of negative growth fits the traditional textbook definition of a recession. While various bodies, including the White House, have sought to redefine the word ‘recession’ (for reasons likely not entirely connected with statistical accuracy) it appears that, at the very least, the US has entered a ‘technical recession’. Indeed, a recession may be what is required to tame inflation.

There is an important discussion that will play out now in investment committees, board rooms and on the airwaves, as to whether we are in a ‘real’ recession and what it means when nominal GDP continues to grow (thanks to high levels of inflation) even as real GDP shrinks. However, today we are focusing on what happens to stock market returns after an economy enters a recession which meets the textbook definition of two quarters of negative growth.

The Start of a Recession is Historically a Strong Signal for Stock Market Returns:

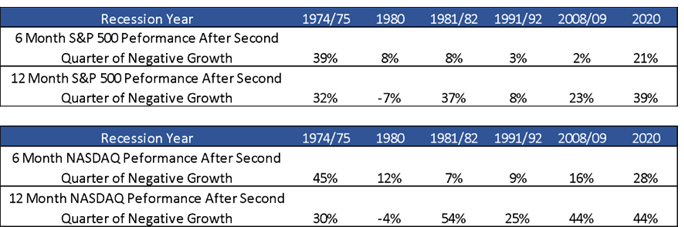

There have been 6 recessions over the past 50 years, using the technical definition of a recession being at least two quarters of negative real growth. Analysis stock market return data shows that performance from when a technical recession is announced, is consistently positive on a six month and twelve month basis. The only exception here being the twelve month performance in 1980.

On a gut level such performance may seem counter intuitive, however it makes logical sense. Recessions seldom happen all at once. By the time an economy has finished the second quarter of contraction companies have already started adjusting their spending, battening down the hatches and moderating workforces. As such the market has had ample time to discount and price-in an oncoming recession.

Secondly, recessions, unlike bull markets, are not usually long drawn-out affairs. They typically last two to four quarters. Therefore once a recession is measured (at the end of the second quarter) we are generally much closer to the end of a recession than the beginning. The longest recession in our data-set was the ‘Great Recession’ triggered by the 2008/09 financial crisis, which lasted for four quarters. Even after this ‘mother of all recessions’, we still saw the S&P 500 index up on both a six and twelve month basis after the recession was confirmed by a second quarter of negative growth.

“It is always darkest just before the Day dawneth.”

Thomas Fuller (1650)

The proverb “it is always darkest before the dawn” is four centuries old. It has persisted so long because it is axiomatic of human behaviour. Historical data shows that, in the case of recessions, the idiom also holds true for markets, which reflect the future expectations of investors. Thus, markets start to price recessions before they happen, likewise they start to price recoveries before they happen, even as recessions are ongoing.